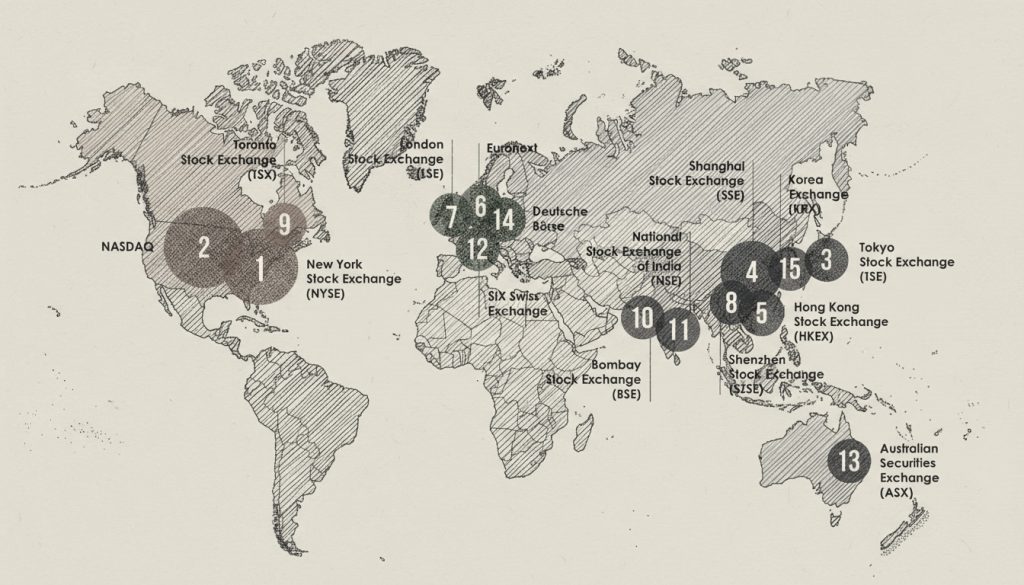

The global landscape of stock exchanges is a mosaic of dynamic financial ecosystems, each influenced by regional economic conditions, regulatory frameworks, and cultural peculiarities. Understanding the interplay of these exchanges provides insight into international trading volumes, investment flows, and market efficiencies across geographical borders.

The United States stands as the titan of global stock trading, predominantly through its two main exchanges: the New York Stock Exchange and the NASDAQ. As of 2025, these exchanges collectively have a market capitalization exceeding $80 trillion, representing approximately 52% of the world’s total stock market value. The U.S. market is characterized by an astounding daily trading volume that frequently surpasses $110 billion. This liquidity attracts foreign investments and provides American companies with immense visibility on the global stage. The U.S. also leads in technological innovation within trading systems, with high-frequency trading algorithms and real-time analytical tools creating a robust trading environment. Furthermore, regulatory bodies like the Securities and Exchange Commission foster transparency and investor protection, fortifying the U.S. as a safe haven for capital investment.

Europe presents a diverse array of stock exchanges, the most significant being the London Stock Exchange, Euronext, and the Frankfurt Stock Exchange. While the LSE is traditionally seen as a hub for international listings, the European stock markets together account for approximately 12% of global market capitalization. However, trading volumes are often fragmented across multiple exchanges due to varying regulatory regimes and market practices. In the wake of Brexit, the LSE faces new challenges, particularly in retaining and attracting foreign listings; the movement of firms to Amsterdam highlights potential shifts in trading volume dynamics. Despite this fragmentation, innovations such as the MiFID II regulations aim to enhance market transparency and efficiency, potentially propelling higher trading volumes in the future.

The nascent stock markets of Africa, led by the Johannesburg Stock Exchange and the Nairobi Securities Exchange, represent the lower end of global trading volumes, contributing less than 1% to the world’s stock market capitalization. The JSE, with a market cap of around $1 trillion, remains the continent’s most robust exchange. Despite the challenges posed by economic volatility and political uncertainty, African exchanges are increasingly adopting technological solutions, like mobile trading and blockchain technologies, to enhance accessibility for retail investors. As intra-African trade develops and foreign direct investment flows increase — particularly in natural resources and technology startups — the growth potential for African stock exchanges is significant.

Asia has several of the largest stock exchanges worldwide, notably the Tokyo Stock Exchange, Hong Kong Stock Exchange, and the Shanghai Stock Exchange. Combined, these exchanges hold roughly 25% of global stock market capitalization, with the HKEX emerging as a key player due to its strategic location for Chinese companies seeking foreign capital. The TSE’s market cap of about $6 trillion signifies Japan’s economic stature, yet trading volumes can be relatively low in contrast to the U.S. and Europe. In contrast, the SSE experiences peaks in trading activity driven by the rapid growth of the Chinese economy, with increasing interest in technology and green energy sectors. However, regulatory constraints and government interventions can create volatility and uncertainty, affecting foreign investment sentiment.

South America, with its burgeoning economies, presents a mixed bag of stock exchanges, with the B3 in Brazil being the most significant player. As of 2025, B3 has a market capitalization of approximately $1 trillion, making it the largest stock exchange in the region. Despite considerable local trading, South America as a whole only accounts for about 2% of global stock market capitalization. Economic fluctuations, often tied to commodity prices, can lead to volatility, but there is rising interest in technology startups and sustainability, which may signal growth potential for the region’s exchanges. Initiatives aimed at improving investor trust and regulatory consistency could foster an environment ripe for investment.

The Middle East’s stock exchanges, centered largely around the Gulf Cooperation Council (GCC) nations, have emerged as significant players on the global stage. The Saudi Stock Exchange (Tadawul) stands out with a market capitalization nearing $2.7 trillion (less than 2% of global stock market capitalization), making it one of the largest bourses in the world. The presence of state-owned enterprises, particularly in oil and gas, adds a layer of stability and growth potential. However, geopolitical tensions and economic diversification strategies are influential factors that shape trading volumes in this region. Efforts to attract foreign investment are evident, particularly through market openness initiatives, which make the Middle Eastern markets increasingly attractive for institutional investment.

In Russia, the Moscow Exchange serves as the primary hub for stock trading, providing access to a wealth of resources, including energy and raw materials. The exchange has a market capitalization of roughly $800 billion. However, the political climate and international sanctions severely affect trading volumes and investor sentiment. While the local economy is resource-driven, venture capital is gradually gaining traction in technology and innovation sectors. The unique blend of resources and challenges makes the Russian stock market an intriguing landscape with potential growth avenues, albeit fraught with risks.

Lastly, the Australian Securities Exchange, while smaller compared to its global counterparts, comprises significant trading volume with a market cap of approximately $2 trillion, contributing roughly 1% to the global market. The ASX is known for its strong performance in resources and financial services, highlighting Australia’s rich mineral wealth and well-regulated financial environment. Recent advancements in sustainable investing and exchange-traded funds have invigorated local trading volumes, reflecting a growing awareness of environmental, social, and corporate governance principles among investors.

The web of global stock exchanges underscores a complex interplay of volume, investors’ propensity to take risks, and regional economic health. While the U.S. retains its crown as the epicenter of trading activity, emerging markets — especially in Asia and Africa — are gradually reshaping the dynamics of international investing. As market participants increasingly engage with these diverse financial ecosystems, the potential for higher trading volumes across all regions remains promising, albeit challenged by local intricacies and global economic shifts.

These regions account for 95% of worldwide stock market capitalization.